Honoring Marvin Goodfriend

Essays related to Marvin and his work:

Essays related to Marvin and his work:

Goodfriend, Marvin. 1991. "Interest Rates and the Conduct of Monetary Policy." Carnegie–Rochester Conference Series on Public Policy 34 (Spring): 7–30.

Marvin Goodfriend's classic 1991 paper, "Interest Rates and the Conduct of Monetary Policy" was first published in the Carnegie-Rochester Conference Series on Public Policy more than three decades ago. It is a wide-ranging paper with an original analysis of interest rate policy that was relevant in 1991 but is even more relevant today. His analysis was informed by his experience in the Federal Reserve System as a policy adviser at the Federal Reserve Bank of Richmond. He took this unique, first-hand experience and translated it into practical monetary policy proposals in a highly thoughtful and original way.

The Goodfriend paper begins with a history of the Fed's interest rate targeting procedures that is useful for monetary economists even today. He then reviews the instrument choice problem — money versus interest rate — that had been studied in a classic article by William Poole in 1970, describing how its results carried over to a modern dynamic-rational-expectations model. He discusses the mechanics of interest rate smoothing, showing how the persistence of the federal funds rate results from the Fed's macroeconomic stabilization policy.1 Finally, he provides evidence that the Fed implicitly had rules-based monetary policy for the interest rate during most of the 1970s and 1980s.2

In this paper, I build on the analysis of Marvin Goodfriend and examine how the Fed can better engage in a rules-based monetary policy going forward.

Prior to the global financial crisis, policymakers within the Federal Reserve System had adopted elements of the rules-based approach to interest rate policy that I advocated in my 1993 Carnegie-Rochester paper. For example, during his time as president of the Federal Reserve Bank of St. Louis, William Poole used "the Taylor rule" as a guide to his thinking about policy actions to be taken in upcoming meetings and as a vehicle for explaining the Fed's decisions to the public.3 But then there was a move away from such an explicit use as the Fed and the government more generally used a wide range of policies to deal with the Great Recession, not all of which I view as desirable.4

More recently, starting around 2017, the Federal Reserve returned to a more rules-based monetary policy that had worked well in the United States in the 1980s and 1990s, as Goodfriend observed. Many papers were written at the Fed and elsewhere reflecting this revival and showing the benefits of rules-based policies. In 2017, the Fed began to report on rules-based policy in its Monetary Policy Report, and favorable comments about rules-based policy were made by many policymakers.

One explanation for the revival was simply a revealed preference for such an approach on the part of monetary policy officials and others interested in monetary policymaking. Another explanation for the revival was the desire to figure out how to deal with the effective or zero lower bound on the interest rate that Goodfriend (2000) had highlighted earlier: there was genuine concern at the Fed about the lower bound in the case of a need for substantial easing. Another possible explanation was the disappointment with monetary policy leading to the Great Recession and especially the deviation from rules in the 2003-05 "too low for too long" period. Yet another explanation was the recognition that rules are needed to evaluate quantitative easing proposals.

The Fed began a helpful reporting approach in the July 2017 Monetary Policy Report when Janet Yellen was Fed chair. Each report contained the policy rate implications of five well-known rules embedding reactions to inflation and unemployment.

However, that move toward rules-based policies was interrupted when COVID-19 hit the American economy. The Fed took a number of actions to deal with the economic effects of the severe health crisis.5 By most accounts, these actions were special and were not consistent with rules-based policies.

The Fed also stopped reporting on rules-based policy in its Monetary Policy Report. The pandemic that started in the first quarter of 2020 was a jolt to the American economy and to many other economies. It interrupted the revival of rules-based policies at the Fed and most other central banks. The actions at the Fed included a rapid reduction in the target for the federal funds rate from 1.75 percent to .25 percent during the weeks of March 2020. Both M1 and M2 measures of the money supply grew rapidly. It also included large-scale purchases of Treasury and mortgage-backed securities, causing a large expansion of the Fed's balance sheet with assets rising rapidly from about $4 trillion to about $7 trillion during the second quarter of 2020 and then continuing to grow to about $9 trillion at the end of 2021.

The Federal Reserve's Monetary Policy Report after the first year of the pandemic, released on February 19, 2021, however, contained a whole section on monetary policy rules. That policy rules reentered the Report was a welcome development, restoring the helpful reporting approach from the July 2017 Monetary Policy Report. The approach continued in 2018, 2019, and early 2020, but it was dropped in July 2020.

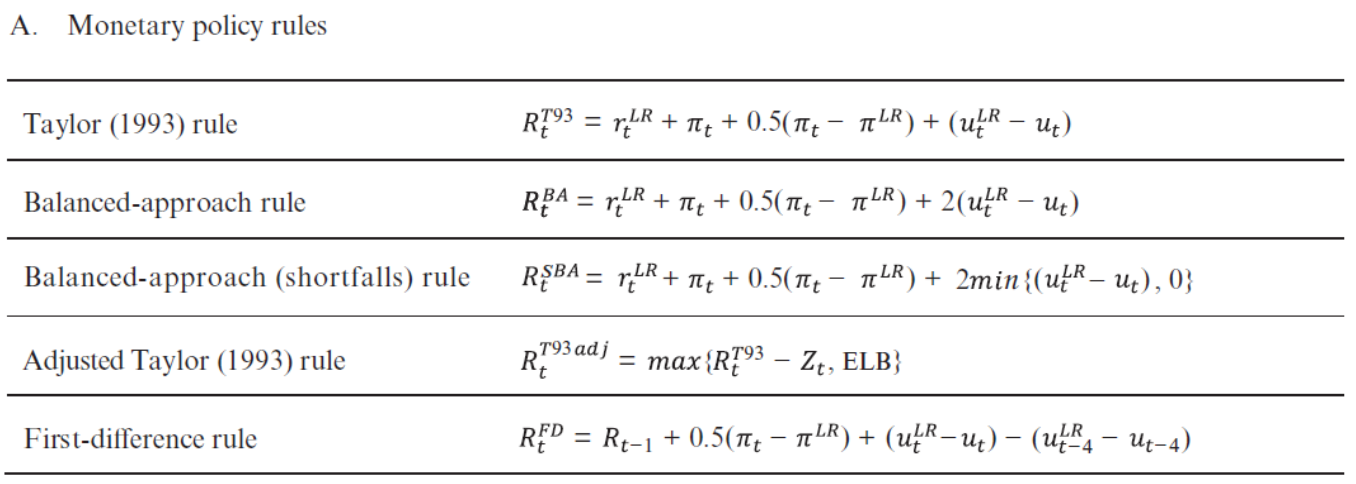

Five rules were discussed in the February 2021 Monetary Policy Report on pages 45 through 48. To quote the Report, these include "the well-known Taylor (1993) rule, the 'balanced approach' rule, the 'adjusted Taylor (1993)' rule, and the 'first difference' rule." In addition to these rules, there was a new "'balanced approach (shortfalls) rule,' which represents one simple way to illustrate the Committee's focus on shortfalls from maximum employment." Table 1 shows the five rules from the February 2021 Report. There were also five rules in the earlier Reports, but the February Report left one out and added the new balanced approach (shortfalls) rule in its place. As stated in the Fed document, this simple new rule would not call for increasing the policy rate as employment moves higher and unemployment drops below its estimated longer-run level. This modified rule aims to illustrate, in a simple way, the Committee's focus on shortfalls of employment from assessments of its maximum level.

Dotsey, Hornstein and Wolman discuss Goodfriend's (1987) modeling of interest rate smoothing in another essay in this volume.

Athanasios Orphanides and Volker Wieland later provided a detailed confirmation of this view, stimulated by their work at the Fed to provide "Taylor Rule" memos to the FOMC starting in the mid 1990s.

See Poole (2007).

Taylor (2009).

See Taylor (2021).

In 2013, Andrew Levin and I argued that "getting behind the curve" was central to the Great Inflation of the 1960s and 1970s.